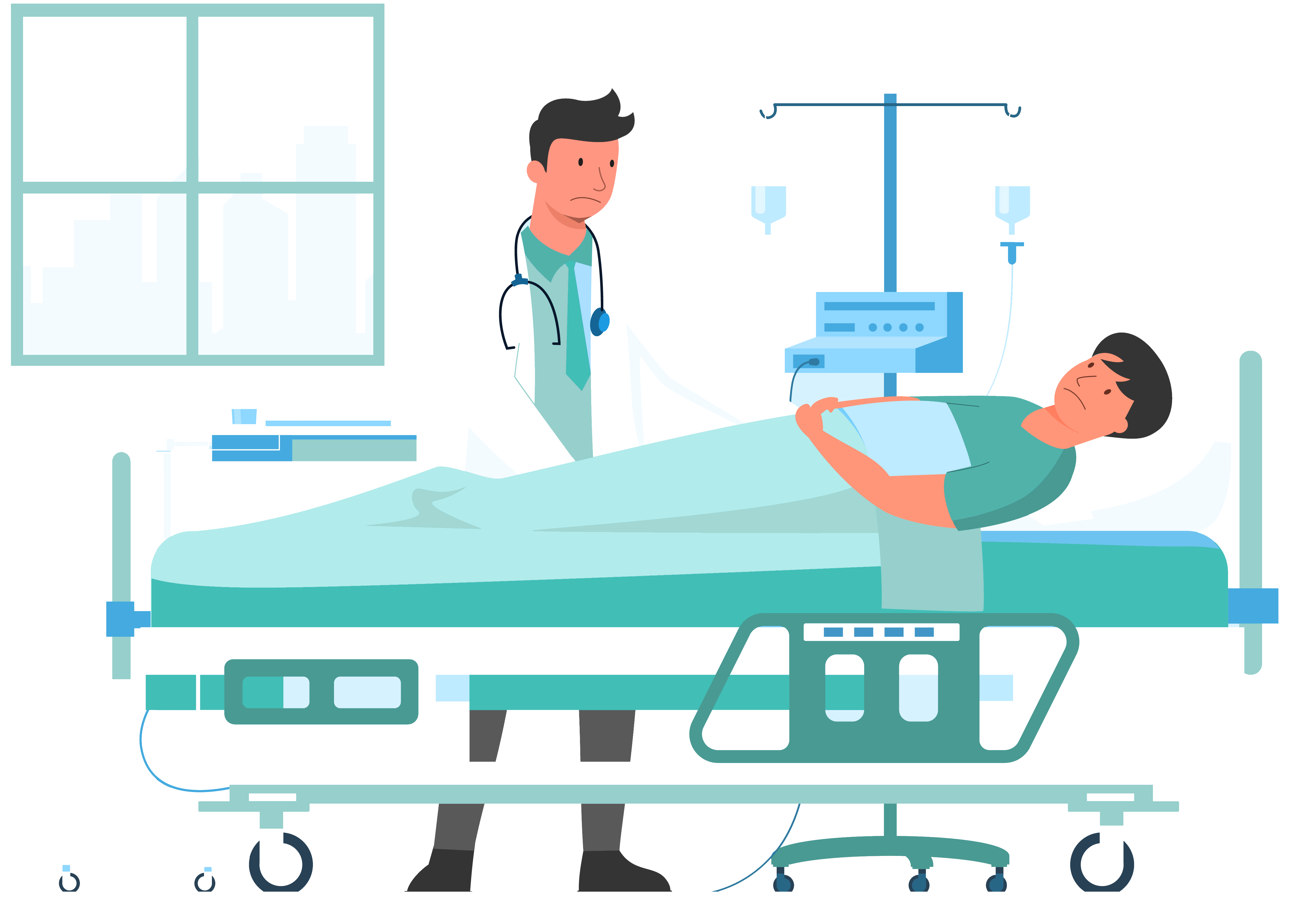

The possibility of high value health Insurance

claims has increased. Exponentially.

Remember the Medical expenses under Covid?

Claims of 25 lacs became very common.

Other Scenarios where high hospital bills became a reality.

Future

Pandemics

Future

Pandemics  Poisoning cases,

Poisoning cases, Liver

Transplants

Liver

Transplants Sepsis.

Sepsis.

Road

Accidents.

Road

Accidents.  Kidney

Transplants

Kidney

Transplants  Lung

Infections

Lung

Infections  Cancer

Treatments.

Cancer

Treatments.

Advance treatments like Stem Cell.

Advance treatments like Stem Cell.